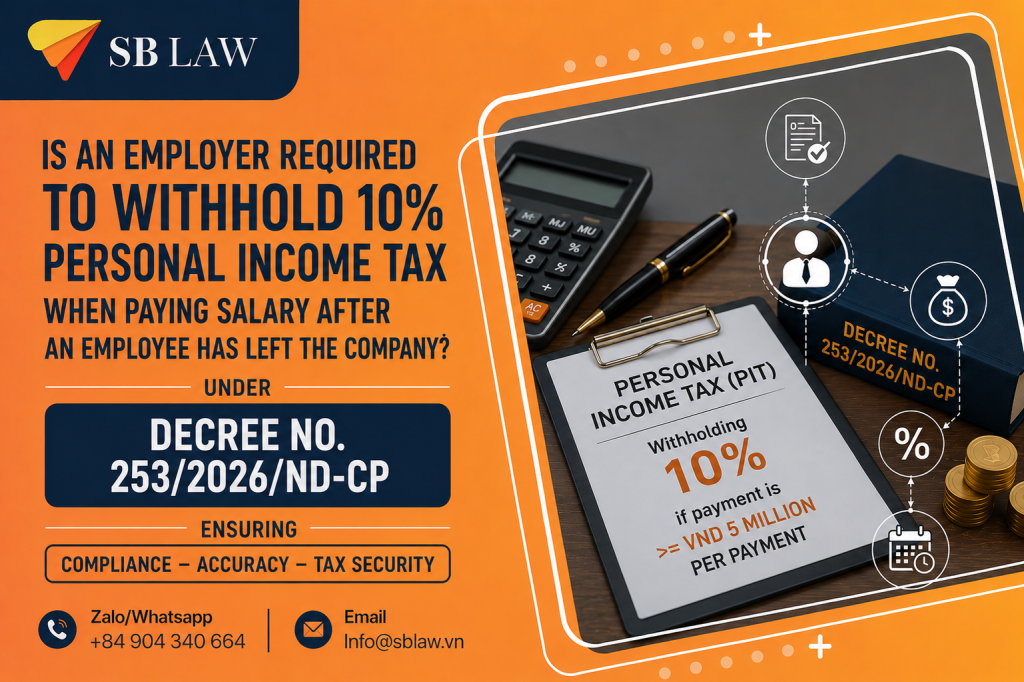

Question: Is an employer required to withhold 10% personal income tax (PIT) when paying salary to an employee after the employment contract has been terminated? Answer: Under Clause 2, Article 50 of Decree No. 253/2026/ND-CP, where an employer pays salary, wages, or other income to an employee after the employment contract has been […]